Building the Foundation for Downtown in 2006 and 2007

Policy advancements and putting Tax Allocation Districts to a vote

After the 2005 Town Center Master Plan and Land Use Amendment, the work of moving forward on making downtown a reality began.

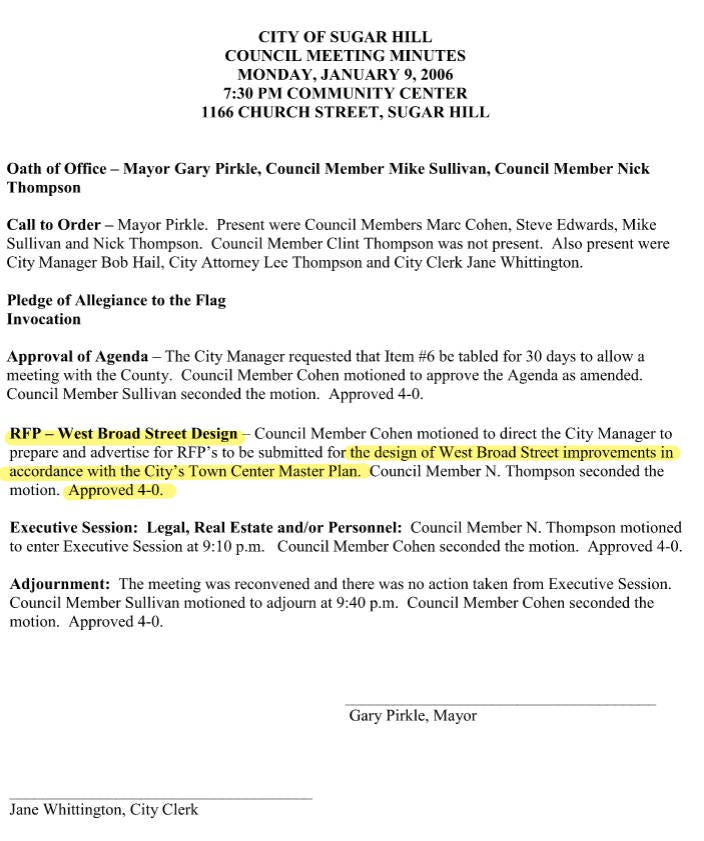

The first order of business were improvements to the city’s main street - West Broad Street. The design process would begin in January 2006.

The award of the design contract would happen a few months later in April 2006 to a local Gwinnett County engineering firm Pond & Company.

Finally, with the design complete, it would be approved in December 2006 and the city would move forward with right-of-way acquisition for the improvements for West Broad Street.

Next up in January 2007 was one of the more important decisions that the city made with regard to realizing downtown - the decision to put a Tax Allocation District (TAD) up to a vote by city residents.

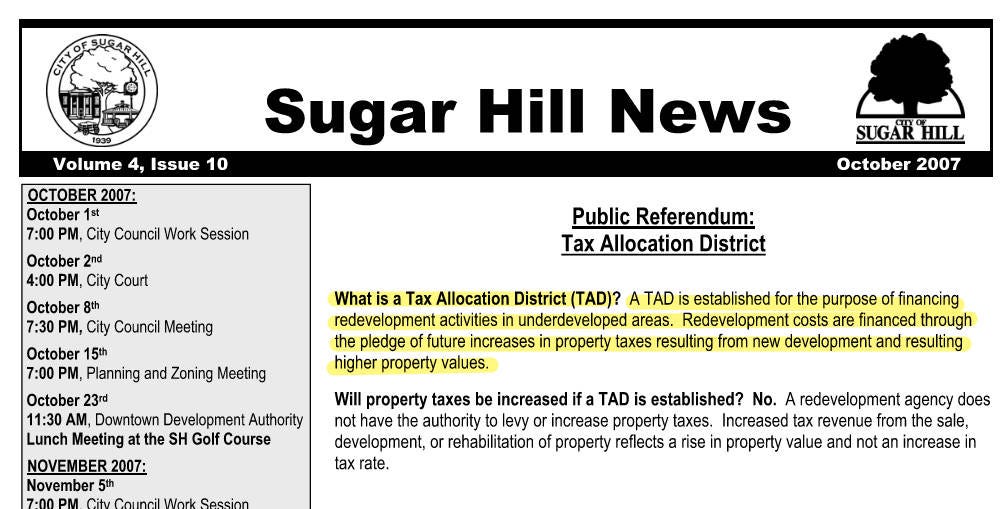

First, let’s discuss what a TAD is - here’s what the city put out in an October 2007 newsletter.

Below is a commonly used chart to help explain a TAD.

AV above stands for “Assessed Value” - the value on which property is taxed. When a project uses a TAD, the property’s assessed taxable value is frozen for the life of the TAD for property tax payments (frozen at the property’s base value prior to the project - in purple in the chart). As the project is built and its assessed value increases, the difference between the property taxes that would have been paid without the TAD versus the base value is allocated to the project costs (yellow in the chart). Often, those are bonds associated with public infrastructure.

At the end of the TAD, the project then goes onto the tax digest at current assessed value and no longer has the ability to credit the property tax difference to the project costs (orange in the chart). Some might say it’s a tax abatement but that isn’t really an accurate term for it - tax abatement would imply the developer is pocketing the difference, which is not the case. Rather, the tax difference is going to the project costs, which are often bond payments. Where that money goes is spelled out at the beginning of the TAD.

Here’s additional information on TADs from the Georgia Main Street Program.

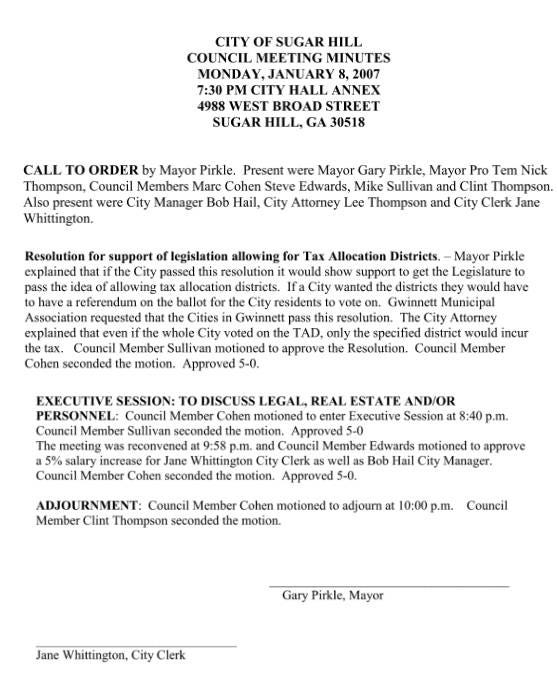

The decision to put a TAD on the ballot was made in January 2007. Below are the minutes from the meeting in which Mayor and Council supported state legislation that would allow for a referendum on a TAD.

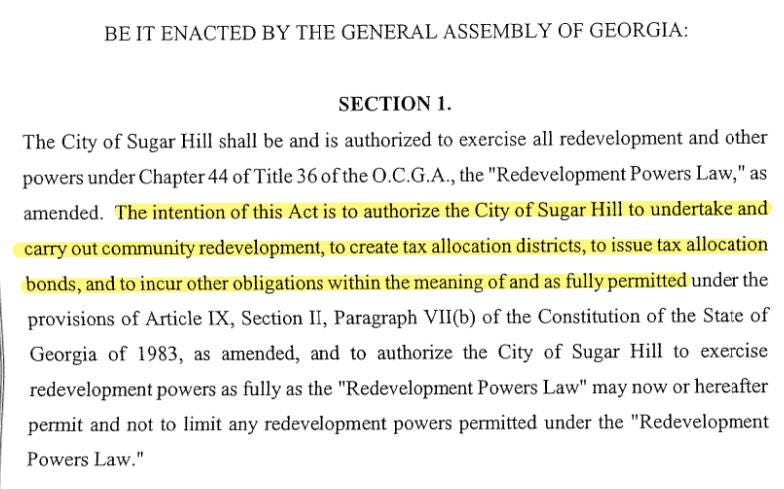

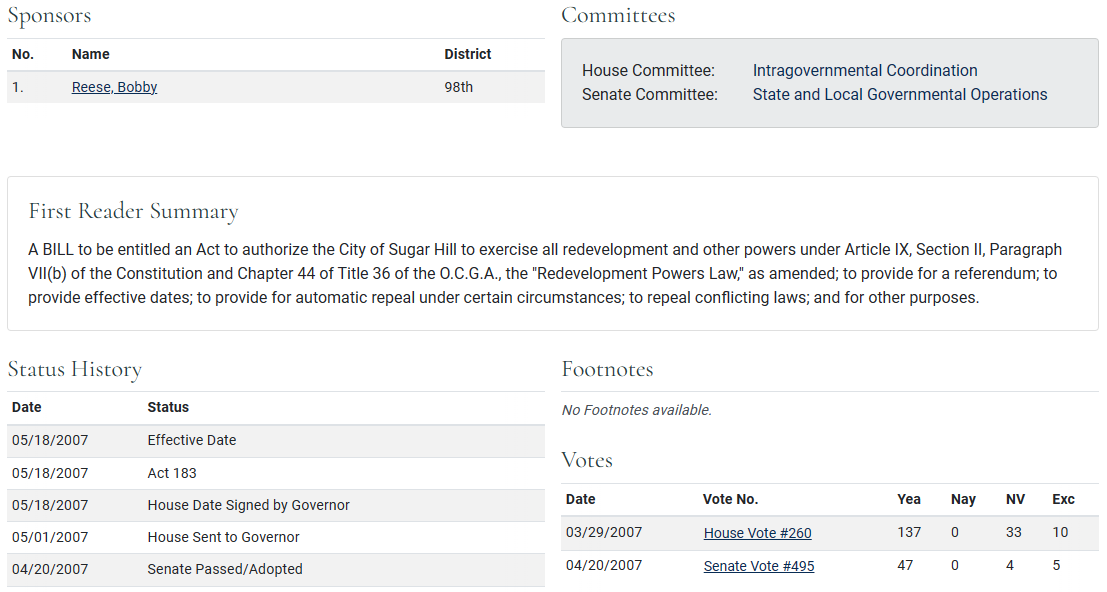

The importance of this passing in January 2007 is that it allowed time for the state legislature to pass the required state legislation to allow for the local referendum. This took the form of House Bill 746 sponsored by then 98th district (the district that represented the vast majority of Sugar Hill at that time) Representative Bobby Reese during the 2007 legislative session. The important portion of that bill is below.

The bill would go on to pass both the House and Senate unanimously.

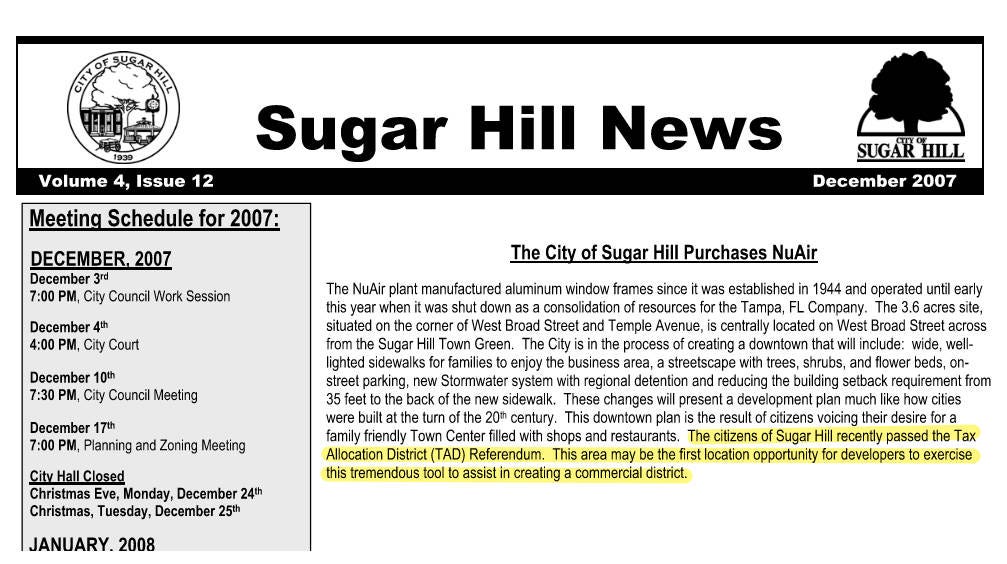

As a result, a TAD referendum was placed on the November 2007 ballot for the citizens of Sugar Hill to decide if they wanted to allow a TAD in Sugar Hill. The referendum would go on to pass the city referendum with 70% voting in favor. The city noted the passage in the December 2007 edition of the Sugar Hill News stating, “This area [downtown] may be the first location opportunity for developers to exercise this tremendous [emphasis mine] tool to assist in creating a commercial district.”

Also of importance in this same newsletter is the city’s purchase of the shuttered NuAir facility where city hall now stands along with comments on a future downtown.

Access WDUN and the Council for Quality Growth noted the passage at the time - TADs passed in all 9 Gwinnett County cities that it was on the ballot.

The importance of the TAD passing can’t be understated. It was the authorizing legislation for what would allow for the development and realization of downtown by incentivizing development through the ability to use property tax growth from the city, county and schools to be put back into the project for a period of time. To recap the votes: it was unanimously supported by city council, unanimously supported by the state legislature and overwhelmingly supported by Sugar Hill citizens when put to a vote.

To date, TADs have not been utilized yet due to Gwinnett County Public Schools unwillingness to agree to the TAD for their portion of the property taxes. Even though GCPS has expressed support for the city’s development, GCPS has been reluctant to support any TADs because of fear of support for one meant support for all. This will be explored further in a future article, but the workaround that has been used throughout the state is a virtually similar mechanism from a property tax standpoint to a TAD called a usufruct. If you want to get really wonky on policy, here is a slide presentation from UGA on it and another presentation from ACCG on it.

Basically, in a usufruct the city’s Downtown Development Authority (DDA) owns the property and project, making it tax exempt. The DDA leases the project back to the developer through a usufruct agreement in which the developer pays the DDA a fee along with any other negotiated concessions, typically having to do with public infrastructure like building public parking decks. There are two projects in Sugar Hill with such an agreement - the Holbrook and Solis, both downtown projects and both of which the fees paid by the developer will exceed what they would have paid in city taxes during the life of the usufruct. We’ll explore those usufructs and projects in a future article as that falls out of the scope of this article.

Towards the latter half of 2007, the city undertook a Community Assessment in preparation for the 2008 Comprehensive Plan update. We’ll cover both in a separate upcoming article.

The two years following the initial downtown master plan and land use amendment saw major moves forward for downtown - West Broad Street design changes and a major policy initiative for the development of downtown. The foundation for downtown, although just a few years in, was getting stronger.